The positive impact of AI for insurance companies

The way customers communicate with companies has shifted. From a customer viewpoint, calling a customer service line or sending an email is outdated, often leaving them frustrated and without an immediate solution.

In today’s digital-first world, machine-based solutions are readily available and heavily adopted by companies across numerous industries, helping their customers quickly find the necessary information they need.

The insurance sector is notoriously slow to evolve, but AI for insurance provides convenience and the expansion of customer service opportunities, as well as the chance to provide streamlined interactions with more personalised solutions.

Because of the benefits seen across numerous sectors, Insurance companies are now investing heavily into AI technologies.

However, it’s also proving to be valuable in numerous fields, including retail, medical training, e-commerce and employee development. For some, it’s even a useful tool to treat anxiety, which shows that VR can be used in an endless and varied number of ways. As we’ve mentioned, not only can this technology be used by the people, but also businesses – so here are our top 6 VR companies to watch this 2022 (in no particular order).

How the market environment evolved

The stagnation of customer-based offerings supplied by insurers was already apparent in the pre-pandemic world. Since then, web and app based services have accelerated, and the industry has had to adapt to customers being familiar with AI backed solutions.

Pre-pandemic, insurance companies were already struggling with sluggish growth rates. Research by McKinsey highlighted glaring inadequacies in the insurance industry, showing the sector had fallen behind many others:

“In today’s digital and rapidly changing market environment, insurers must take a more aggressive, structural approach to reduce complexity and enhance productivity. Beyond efficiency, both the effectiveness of individual processes (such as in underwriting or claims) and an excellent customer experience in all interactions are core parts of the new equation.”

AI for insurance

Insurers need to provide an agile process for each consumer and their respective customer service journey. This is where AI can help insurers focus on concerns or issues that frequently occur, using a customer’s data to pull together a detailed picture of the issues they face the most.

Why investment in AI is growing in the insurance industry

Increase of data accuracy

Efficiency and accuracy in the insurance sector is critical. As such, AI-based tools can assist in processing and analysing large data sets, helping insurers formulate a better understanding of the individual and their claim.

While it can take a human agent several minutes to analyse and cross reference data, AI tools can do this instantly and relay the data back to the human to make an informed choice.

Armed with more accurate insights and knowledge, insurers are better equipped to put together a product for customers that increases reliability and reduces problems when customers eventually make a claim or decide to renew.

Reduction of human error

As AI (and intelligent self-service tools) become commonplace across industries, companies need to address this by realigning the roles of their employees. Upskilling staff to leverage these AI tools will create more opportunities for growth, both for the individual and company.

By deflecting simple tasks and queries that can be solved by an automated-AI tool, the role of customer service agents can evolve to focus more on nurturing customer relationships and building loyalty and reliability within the customer base.

A report by Genpact discussed how AI would create an augmented workforce:

“AI will augment workers’ skills, freeing them up to focus their expertise and judgement on complex risks, and their empathy and emotional intelligence on customer experiences. Excited by the promise of applying technology to real-time risks, insurers will attract a new breed of talent to the industry.”

When you consider most customers only interact with their insurance provider when somethings gone wrong or they need to make a claim, it’s likely they are already frustrated. Therefore, freeing up staff who can offer a more empathetic response is a great way to de-escalate problems and turn the experience into a positive one.

Augmented workforce

Customers are expected to provide insurers with detailed, accurate information about themselves, which is then passed through a series of underwriters and examiners. However this isn’t foolproof. Customers can often unintentionally supply inaccurate information, which can cause problems or delays during the claims process and identifying the level of risk to insurers.

AI-assisted risk assessments and tailored plans that suit the needs of each customer are beneficial. By reducing human error throughout the application process, customers are more likely to purchase insurance policies that meet their specific needs. For example, not paying for more coverage than required or coverage not actually needed.

Ultimately, customers receive what they require.

Why investment in AI is growing in the insurance industry

AI can simplify processes across many different insurance sectors. Fraudulent claims, processing of claims and underwriting are all obvious areas that can be improved with AI.

But as more tasks become automated, insurers can quickly scale the amount of claims they can process without human intervention, creating quick, seamless interactions.

This is what modern customers demand. They no longer tolerate lengthy processes that send them on complex journeys through various touchpoints. Customers now expect simplified interactions that help solve their issues quickly and efficiently.

To keep up with these demands, insurers must adapt their offerings. Below, we look at 3 examples of how artificial intelligence is being used within different insurance sectors.

AI in Health Insurance

The health insurance sector is being transformed by AI technology, as the opportunities provided by wearable devices expand. The constant data feedback provided by these devices gives insurers a window into users’ health. For example, how active they are, their heart rate, their location, and more.

The relationship between Apple and healthcare insurance provider Aetna is a great case study.

Apple and Aetna partnered to launch the Attain app, which leverages Apple Watch data to provide an insight into the health of its users. Users have the benefit of reporting live health data, while Aetena can quickly react to concerns and offer better health guidance for users. As healthcare moves towards these more personalised approaches, leveraging data through AI will become critical.

Already doing this is health insurance company Cigna, who uses AI to monitor health data and personalise treatments. Using Prognos Health, they provide health monitoring by using AI to predict if an individual is at risk of a certain disease.

Cigna uses data and software to inform members of any developments in their health drawn from the data, which provides earlier intervention, safeguards potential health risks and reduces incurred costs for members as a result.

AI in Life Insurance

This approach can be applied to life insurers, as their ability to meet demands of customers is made much easier through AI supported processes.

Personalised pricing, disease severity prediction, submission prioritising, and quick product creation are all key components that AI can help deliver for life insurance underwriting.

AI in Car Insurance

Car insurers still spend hours processing documents manually, via legacy software that is slow and outdated. But the sometimes life and death nature of auto insurance requires insurers to consider every minute aspect of a car, such as the development in safety technology. It is not enough for insurance premiums to be calculated by vehicle size alone.

However, fraudulent claims are a huge threat and the need for accuracy is crucial. Is the driver misrepresenting details, the car’s usage or the events that led to an accident?

Despite this, drivers are reluctant to opt for the little black boxes that monitor your driving. Even when it saves them money.

So while monitoring driving data is possible, a better way of accessing risk could follow the example of the Attain app. By monitoring the car’s health, insurers can better access risk, check policies and limits, and track losses or damages.

Data like time since last tyre change or last break change, combined with mileage data submitted by the user (or even MOT data), gives insurers more data to provide personalised coverage with. It also strengthens a drivers case, should they need to claim.

Meanwhile, AI can also be used to identify motor insurance fraud, as AI can quickly cross reference data to ensure claims comply with the coverage purchased. For example, if a driver submits an accident claim on their work only vehicle but the accident happens far from the place of work, it can flag the case for a human to review.

Inversely, if all the data is accurate drivers can complete their claim without a human intervening, creating quicker claims processes.

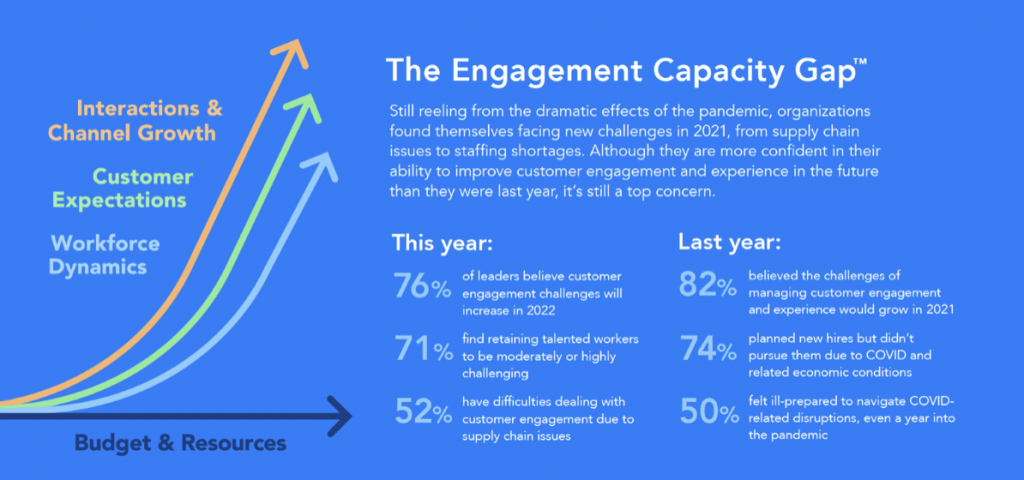

Closing the engagement capacity gap

There is a chasm between what insurers know they need to do to meet rising customer expectations and the resources they have to do it. Both in terms of budgets and human resources, they are having to figure out ways to anticipate the rising demands of consumers and how best to apply the resources they do have in order to meet this demand.

Particularly in the post-pandemic landscape where budgets have been slashed. The graphic below outlines the causes of the engagement capacity gap, and how insurers must adapt to confront this.

Insurers that are focusing on implementing AI are helping to combat the new challenges, such as supply chain issues and staff shortages.

As demonstrated by Verint’s research, understanding customers’ needs is the biggest challenge companies face. As demands and expectations change, insurers need to anticipate what their customers want – efficient, solution-based, and empathetic customer service.

What we’ll see over the next few years is the insurance companies who invest in AI gaining more market share by simply providing a refined customer experience that helps bridge that all-important engagement capacity gap.

The future of AI for insurance

While some insurance companies have restrategised and embraced the digital change, many companies have only partially invested in AI (most have simple triage chatbots). This is partly due to historical financial burdens, such as resources being poured into legacy systems they are now saddled with.

Despite this, significant future investment in AI will be required, even if additional costs are to be incurred short term, as the long-term benefits will offset the short-term investment through increased productivity, adaptation in workforce skills and remaining competitive within the industry.

AI is undoubtedly helping to transform the insurance sector, enabling the growth while meeting the expectations of customers and providing greater transparency.

However, further advancements are imminent, and the use cases for insurance AI are becoming more apparent. The insurance companies that pivot towards digitally-focused customer service experiences will only increase their operational effectiveness and customer satisfaction rates.

Find out more about how to create convenient customer interactions with our free webinar: “Intelligent Self-Service: The Age Of Convenience”. Download below: